Why rates under 6% aren't fixing whats actually broken

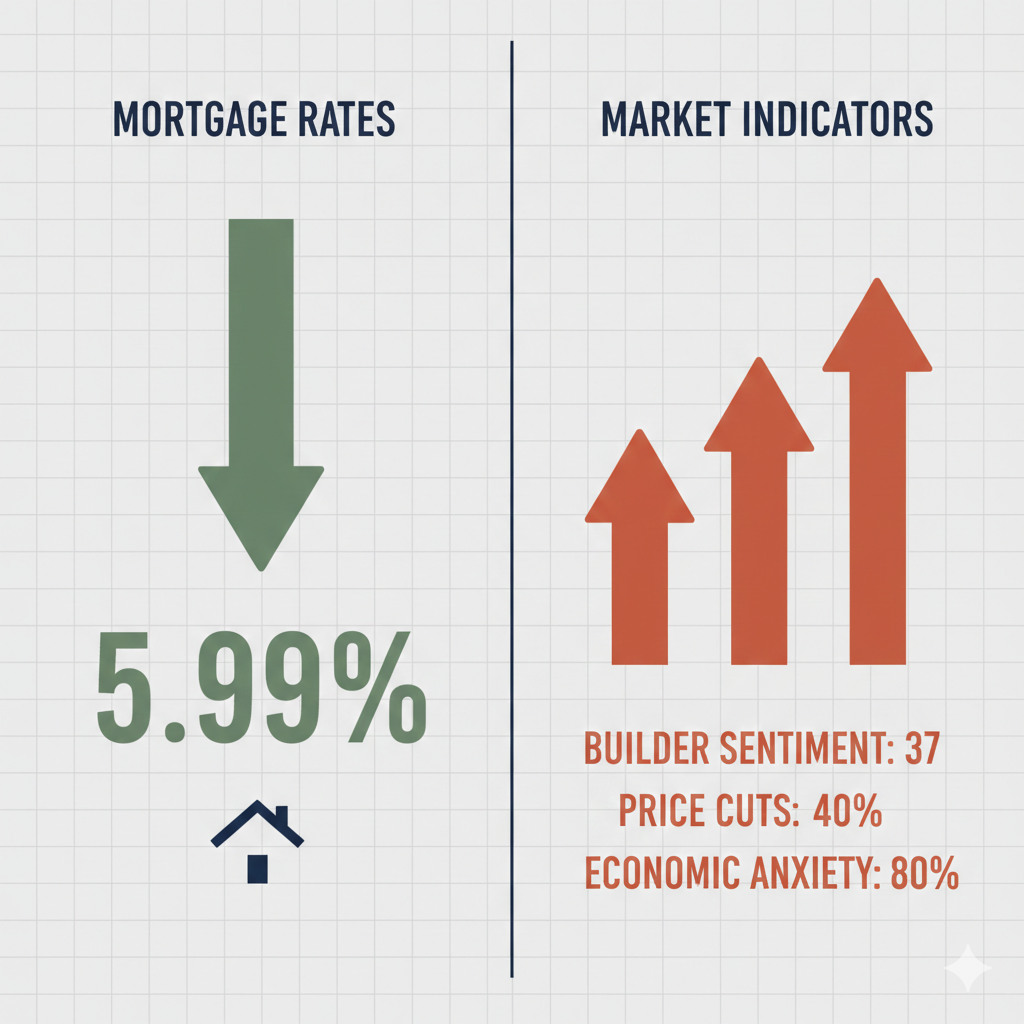

Mortgage rates broke below 6% this week for the first time since September 2022. Refinance applications jumped 40% in a week. The headlines are bullish.

But if you’re an agent waiting for this to unlock a flood of buyers, you’re gonna be disappointed.

Here’s what’s actually happening.

The Rate Drop Isn’t Market-Driven

Rates didn’t fall because the Fed cut or because inflation cooled or because bond markets decided housing was a great bet again.

They fell because President Trump directed Fannie Mae and Freddie Mac to buy $200 billion in mortgage-backed securities.

That’s not stimulus. That’s market intervention.

Fannie and Freddie were already buying MBS at a 77% annualized pace over the last six months. Trump pushed them harder. They buy more, demand goes up, yields compress, mortgage rates drop.

Simple math. But it’s not organic.

And here’s why that matters: Fannie and Freddie holding massive portfolios of mortgage-backed securities is exactly what contributed to their collapse in 2008. Yeah, underwriting standards are way better now. But the principle’s uncomfortable.

The government’s using GSE cash reserves to artificially lower housing costs right before midterms. Call it what it is.

The Refi Spike’s Real But Temporary

Refinance applications jumped 128% year-over-year. People locked at 7% are grabbing 5.9%. Smart move.

But refi booms don’t last. We’ve seen this pattern all year. Rates dip, refi activity spikes, rates stabilize, activity drops back.

And purchase activity? Not moving the same way. First-time buyers are still stuck. Economic anxiety’s still real. Lower rates help, but they don’t fix affordability when median home prices are elevated and down payments are brutal.

Builder Sentiment Dropped to 37

NAHB Housing Market Index fell to 37 in January. That’s below 50 for the 21st straight month.

Upper-end housing? Holding steady. Buyers at that level aren’t rate-sensitive. They’re moving.

But lower and mid-range? Getting crushed.

Forty percent of builders are cutting prices. Average reduction: 6%. Sixty-five percent are using sales incentives. Those numbers don’t signal confidence. They signal desperation to move inventory.

And here’s the weird part: new homes are now cheaper than the median resale home. That almost never happens.

It’s a combination of where builders are putting inventory (affordable markets like the Midwest, not coastal cities), aggressive incentives, and the fact that resale inventory’s still constrained enough to keep prices sticky.

But don’t mistake builder discounts for a healthy market. They’re sitting on inventory they can’t move at asking.

Economic Anxiety’s the Real Problem

Over 80% of renters surveyed said they’re worried about cutting essential spending. Not discretionary stuff. Essentials.

That’s not a housing market issue. That’s a demand issue.

The “K-shaped economy” everyone talked about in 2025? Still here. High-income buyers are active. Everyone else is cautious or tapped out.

Rates under 6% help buyers who can already afford to buy. They don’t unlock the marginal buyer who’s worried about job security or savings.

What This Means for Positioning

Stop waiting for rates to fix demand. They won’t.

If you’re working luxury, rates don’t matter much anyway. Keep doing what you’re doing.

If you’re working entry-level and mid-range, recognize you’re in a tighter, more cautious market. Builder incentives might be your best angle. New construction’s offering deals you’re not seeing in resale.

And get comfortable explaining value without leaning on market momentum. Buyers are skeptical. They’re not dumb. Lower rates are nice but they’re not fixing the structural stuff that’s keeping people sidelined.

The play isn’t chasing volume. It’s recognizing which segment you’re in and adjusting.